Sustainable retirement income is becoming an important part of workplace retirement planning. For many employees, most retirement education focuses on accumulation—contributing to a workplace plan, selecting investments, and building long-term savings.

However, reaching retirement creates a different set of decisions.

Employees must determine how to convert accumulated savings into reliable income, manage taxation, protect against longevity risk, respond to inflation and market volatility, and coordinate workplace savings with public pensions and personal financial resources.

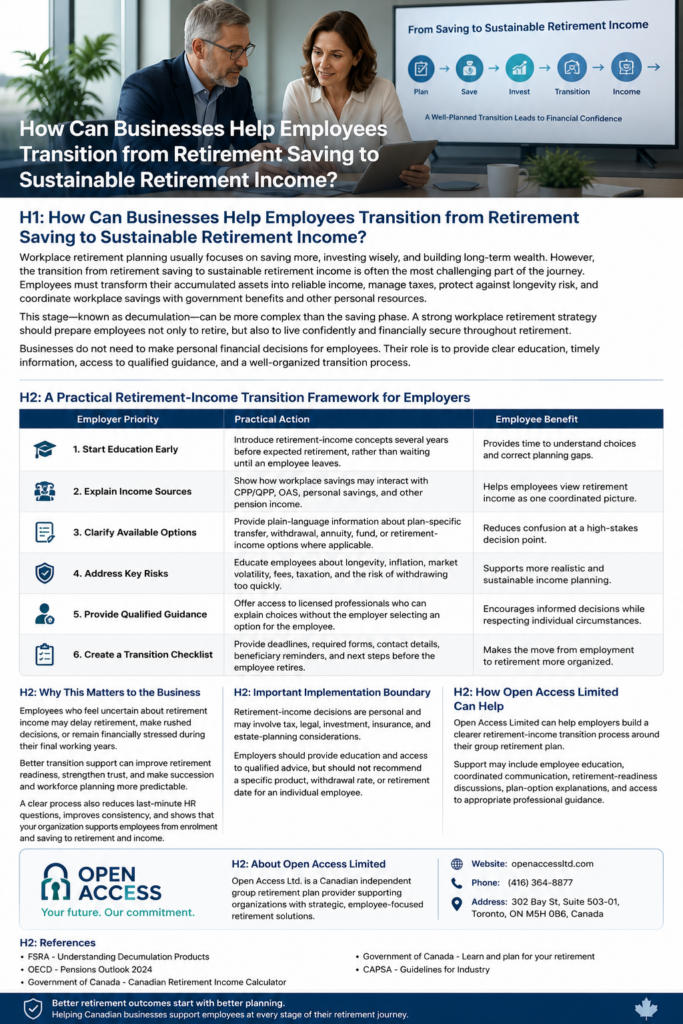

This stage is often called decumulation. It can be more complicated than saving because employees may need to make decisions that affect their financial security for the rest of their lives.

A strong workplace retirement strategy should therefore prepare employees not only to reach retirement, but also to create sustainable retirement income after employment ends.

Businesses do not need to make personal financial decisions for employees. Their role is to provide clear education, timely information, access to qualified guidance, and a well-organized transition process

Why Is the Transition to Sustainable Retirement Income Important?

Employees may spend decades building retirement savings without receiving enough guidance about how those savings will eventually provide income.

Retirement income may come from several sources, including:

- Workplace retirement plans

- CPP or QPP

- Old Age Security

- Personal RRSPs or other savings

- Pension income

- Investment accounts

- Annuities or retirement-income funds

- Other personal or family resources

When these sources are considered separately, employees may find it difficult to understand their complete financial position.

Effective sustainable retirement income planning helps employees view these resources as one coordinated picture.

It also helps employees understand that retirement income must often last for many years while managing inflation, market changes, fees, taxation, health-related costs, and unexpected expenses.

7 Proven Ways Employers Can Support Sustainable Retirement Income

1. Start Retirement-Income Education Early

Retirement-income education should begin several years before an employee expects to retire.

Waiting until an employee submits a retirement notice can create unnecessary pressure. Employees may not have enough time to understand their choices, correct contribution gaps, review beneficiaries, or seek professional advice.

Employers can introduce concepts such as retirement income sources, withdrawal planning, taxation, inflation, longevity, and plan-specific options through workshops, webinars, employee guides, and retirement-readiness discussions.

Early education gives employees time to make informed decisions and prepare for sustainable retirement income gradually.

2. Explain How Different Income Sources Work Together

Employees should understand how workplace retirement savings may interact with CPP or QPP, Old Age Security, personal savings, pension income, and other resources.

Employers should not calculate or recommend an individual retirement-income strategy. However, they can provide general education showing how different income sources may form part of a broader retirement plan.

This helps employees avoid viewing their workplace account as their only source of income.

A coordinated approach can improve financial awareness and help employees ask better questions when speaking with a qualified professional.

3. Clarify Available Retirement-Plan Options

Options

Employees approaching retirement should receive clear, plain-language information about the options available under their specific workplace plan.

Depending on the plan, options may involve:

- Remaining in the existing plan

- Transferring assets

- Moving funds to an eligible retirement-income vehicle

- Purchasing an annuity

- Establishing scheduled withdrawals

- Selecting available fund or income options

- Completing required forms before retirement

Not every option is available under every plan.

Employers should work with their plan provider to ensure information is accurate, timely, and consistent.

Clear explanations can reduce confusion at a high-stakes decision point and support more confident sustainable retirement income planning

4. Educate Employees About Key Retirement Risks

Employees need to understand that retirement-income planning involves several risks.

These may include:

- Longevity risk

- Inflation

- Market volatility

- Investment fees

- Taxation

- Unexpected expenses

- Withdrawing money too quickly

- Holding an unsuitable investment mix

- Failing to update beneficiaries

- Losing track of retirement accounts

Employers can offer general education about these risks without recommending a specific withdrawal rate, investment product, or retirement date.

Risk awareness helps employees understand why sustainable income requires ongoing planning rather than a single decision made on the day they retire.

5. Provide Access to Qualified Professional Guidance

Retirement-income decisions may involve tax, investment, insurance, legal, and estate-planning considerations.

Employers should not select a product or financial strategy for an employee.

Instead, they can provide access to licensed and qualified professionals who are able to discuss individual circumstances.

Professional guidance can help employees understand their available choices, ask appropriate questions, and evaluate how workplace savings fit into their broader retirement goals.

This supports informed decisions while respecting the boundary between employer education and personalized financial advice.

6.Create a Retirement Transition Checklist

A transition checklist can make the move from employment to retirement more organized.

The checklist may include:

- Required forms

- Important deadlines

- Plan-provider contact information

- Beneficiary review reminders

- Personal contact-information updates

- Information about account access

- Available education sessions

- Public pension resources

- Professional guidance contacts

- Next steps after employment ends

Employees should receive this checklist before their final working day.

A clear process can reduce last-minute questions, improve consistency, and help HR teams support employees more efficiently.

7. Continue Support Beyond the Initial Retirement Decision

The transition to sustainable retirement income is not always completed through one meeting or one form.

Employees may need time to review their options, consult family members, speak with professionals, and coordinate several retirement-income sources.

Where appropriate, employers and plan providers can maintain a structured communication process that explains deadlines, account access, and available support.

This does not mean the employer remains responsible for the employee’s personal financial decisions.

It means the organization provides a clear and respectful transition from workplace saving to retirement income.

Why Does Retirement-Income Support Matter to the Business

Employees who feel uncertain about retirement income may postpone retirement, make rushed decisions, or remain financially stressed during their final working years.

Better transition support can improve retirement readiness, strengthen employee confidence, and make succession planning more predictable.

A clear process may also:

- Reduce last-minute HR questions

- Improve communication consistency

- Support workforce planning

- Strengthen trust in the retirement program

- Demonstrate long-term employer support

- Reduce confusion during retirement transitions

Employers that support the complete retirement journey—from enrolment and accumulation to retirement and income—can demonstrate that their workplace plan offers long-term value.

This approach also connects naturally with broader retirement readiness workforce planning strategies.

mportant Implementation Boundaries

Retirement-income decisions are personal.

They may involve taxation, investment management, insurance, pension legislation, estate planning, and family circumstances.

Employers should provide education and access to qualified guidance, but should not recommend:

- A specific investment product

- A particular withdrawal rate

- A retirement date

- An annuity or income fund

- A personal tax strategy

- A specific asset-transfer decision

Plan rules and retirement-income options may also vary depending on the type of workplace retirement plan and the employee’s circumstances.

Employers should coordinate communication with their plan provider and seek appropriate legal, tax, pension, investment, or insurance advice when required.

Strong retirement plan governance can help ensure that employee communication remains accurate, consistent, and appropriately documented.

How Open Access Limited Supports Sustainable Retirement Income

Open Access Limited can help employers create a clearer retirement-income transition process around their group retirement plan.

Support may include:

- Employee retirement education

- Retirement-readiness discussions

- Coordinated plan communication

- Explanations of available plan options

- Transition checklists

- Provider coordination

- Access to appropriate professional guidance

- Employee-focused retirement solutions

Open Access Limited helps employers support employees throughout the full retirement journey—from enrolment and saving to retirement and income.

A structured approach can improve employee understanding, support better decisions, reduce administrative confusion, and help employees prepare for sustainable retirement income.

Open Access Limited

302 Bay Street, Suite 503-01

Toronto, ON M5H 0B6

Canada

Phone: (416) 364-8877

Toll-Free: 1-866-625-4777

Email: inquiry@openaccessltd.com

Website: OpenAccessLtd.com

Final Thoughts

Helping employees transition from retirement saving to sustainable retirement income requires more than providing a workplace savings plan.

Employees need early education, clear explanations of income sources, understandable plan options, risk awareness, professional guidance, and an organized transition process.

Employers should not make personal financial decisions for employees. However, they can create a supportive framework that helps employees understand their choices and prepare for retirement with greater confidence.

A well-designed retirement-income transition process can strengthen retirement readiness, reduce financial stress, support workforce planning, and demonstrate that the organization values employees throughout every stage of their retirement journey.

References

FSRA — Understanding Decumulation Products

https://www.fsrao.ca/

OECD — Pensions Outlook 2024

https://www.oecd.org/

Government of Canada — Canadian Retirement Income Calculator

https://www.canada.ca/en/services/benefits/publicpensions.html

Government of Canada — Learn and Plan for Your Retirement

https://www.canada.ca/en/services/finance/pensions.html

CAPSA — Guidelines for Industry

https://www.capsa-acor.org/